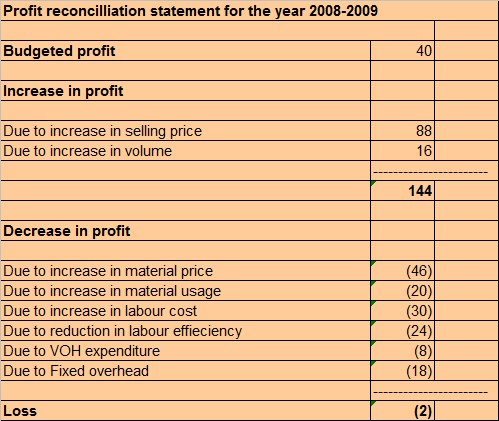

Q. A Company selling consumer durables prepared its budget for 2008-09 anticipating a profit of $ 40 Million. But the actual results for the year disclosed a net loss of $2 Million. The managing director of the company wanted to prepare a statement explaining the reasons for the loss. Details of the budget with actual are given below:-

During investigation you found that there was an overall increase of 10% in cost of material. The labourers were given 15% increase in wages as a result of agreement with trade unions. The selling prices increase by 10%. Prepare a report listing the various factors responsible for the loss of $2 mill. as against the anticipated profit of $40 mill.

Ans.

The increase in selling price = 10%(Given)

As we know that sales is a function of volume and selling price.

Sales = F(Volume,SP)

The actual volume in 2008-2009 without the increase in selling price would be = (968*100)/(100+10) = 880

The increase in SP by 10% contributes purely to increase in profit = 968 - 880 = 88 ---(I)

There is also an actual increase in volume from what was budgeted = 880 - 800 = 80 ----------(i)

Material variances

The material price increased by 10%. (Given)

The material price variance = 506 - (506*100)/(100+10) = 506 - 460 = 46 ---------------(II)

The volume increased by 80 from what was budgeted.

For a volume of 800 the material required = 400

Hence for a volume of 880 , material required would be = (880 * 400)/800 = 440

Thus the material volume variance = 440 - 400 = 40 ------------------------------------------(ii)

The difference 460 - 440 = 20 in material is due to the reduction in efficiency.

Thus the material usage variance = 20 -----------------------------------------------------------(III)

Labour Variances

The labour cost increased by 15% (Given)

The labour price variance = 230 - ((230 * 100)/(100+15)) = 230 - 200 = 30 -----------------(IV)

The volume increased by 80 from what was budgeted.

For a volume of 800 the labour cost = 160

For a volume of 880 the labour cost would be = (880*160)/800 = 176

Thus the labour cost volume variance = 176 - 160 = 16 ------------------------------------------(iii)

The difference 200 - 176 = 24 in labour is due to the reduction in efficiency.

Thus the labour efficiency variance = 24 -------------------------------------------------------------(V)

Variable Overheads

The volume increased by 80 from what was budgeted.

For a volume of 800 the variable overhead = 80

For a volume of 880 the variable overheads would be = (880*80)/800 = 88

Thus the variable overhead volume variance = 88 - 80 = 8 --------------------------------------(iv)

The difference 96 - 88 = 8 in variable overhead is the expenditure variance.

The the variable overhead expenditure variance = 8 -----------------------------------------------(VI)

Fixed Overheads

The fixed overhead variance = 138 - 120 = 18 ------------------------------------------------------(VII)

The increase in volume contributes positively to profit but it also leads to increase in material, labour and variable overhead costs.

Thus from (i), (ii), (iii) & (iv) we see that the increase in profit due to increase in volume is

= 80 – 40 – 16 – 8 = 16

No comments:

Post a Comment